The End of Crucial: How the Memory Industry Is Abandoning the Consumer Market

- Crucial’s role in the PC ecosystem

- Micron’s decision: explicit and strategic

- This is not an isolated case

- Memory pricing is rising, but not for the reasons consumers are told

- What consumers will actually experience

- Revenue follows AI

- Counterargument: what if AI demand slows?

- The hidden risk of over-concentration

- Conclusion: Crucial is a symptom, not the disease

- Sources

For nearly thirty years, Crucial represented a rare constant in consumer technology: reliable RAM and SSDs, fair pricing, and minimal theatrics.

That era is ending.

On 3 December 2025, Micron Technology Inc. (Nasdaq: MU) announced its decision to exit the consumer memory and storage market, discontinuing Crucial-branded products by February 2026.

Shares of the company fell by roughly 2–3% in afternoon trading following the announcement, reflecting short-term market reaction rather than a reassessment of Micron’s long-term fundamentals.

This is not the story of a declining brand.

It is the story of an industry that has decided mass-market hardware is no longer strategic.

Crucial’s role in the PC ecosystem

Founded in 1996 as Micron’s consumer arm, Crucial became a pillar of:

- DIY PC building

- affordable workstation upgrades

- predictable memory compatibility across platforms

Crucial’s competitive advantage was not peak performance, but trust.

For many users, it was the default choice precisely because it removed uncertainty from hardware upgrades.

Its disappearance leaves a structural gap, not merely a branding void.

Clarification: while consumer brands assemble and market memory modules, pricing power and supply control ultimately reside with DRAM and NAND manufacturers. Crucial’s role was downstream; the strategic decision was upstream.

Micron’s decision: explicit and strategic

Micron’s announcement left little room for interpretation.

“The AI-driven growth in the data center has led to a surge in demand for memory and storage.

Micron has made the difficult decision to exit the Crucial consumer business in order to improve supply and support for our larger, strategic customers in faster-growing segments.”— Sumit Sadana, EVP and Chief Business Officer, Micron Technology

Source:

Micron Investor Relations

https://investors.micron.com/news-releases/news-release-details/micron-announces-exit-crucial-consumer-business/

Crucial shipments will continue through Micron’s fiscal Q2 2026, and warranties will be honoured.

However, no further consumer-focused development is planned.

This represents a long-term reallocation of capital, production capacity, and R&D, not a temporary retrenchment.

This is not an isolated case

Micron’s move aligns with a broader industry realignment.

According to Reuters, major memory manufacturers — including Samsung and SK Hynix — are increasingly prioritising high-performance memory for AI and data centres, where margins are structurally higher and contracts are longer-term.

Source:

Reuters, Micron to exit Crucial consumer memory business

https://www.reuters.com/business/micron-exit-crucial-consumer-memory-business-2025-12-03/ The Crucial exit is therefore best understood as a leading indicator, not an anomaly.

Memory pricing is rising, but not for the reasons consumers are told

According to TrendForce analysis published in December 2025, the sharp increase in memory prices projected for Q1 2026 is not driven by a recovery in consumer demand.

Instead, it reflects a deliberate and structural reallocation of supply toward server and AI-centric applications.

Source:

TrendForce via PR Newswire

https://www.prnewswire.com/news-releases/memory-makers-prioritize-server-applications-driving-across-the-board-price-increases-in-1q26-says-trendforce-302652560.html

TrendForce explicitly states that DRAM suppliers are shifting advanced process capacity toward server DRAM and High Bandwidth Memory (HBM) to support AI server deployments. This prioritisation tightens availability across all other segments — including those where demand is flat or weakening.

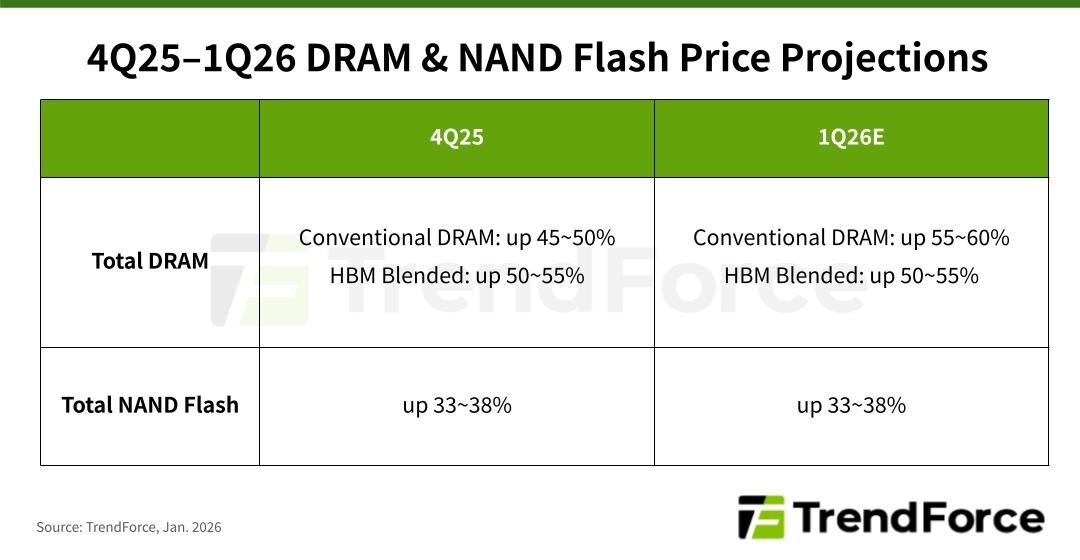

The following graphic from TrendForce summarises projected quarter-on-quarter contract price changes from 4Q25 to 1Q26:

Source: TrendForce / PR Newswire, January 2026

What the data shows

Several dynamics are immediately visible:

- Conventional DRAM prices accelerate from roughly 45–50% QoQ in 4Q25 to 55–60% QoQ in 1Q26, despite weak notebook and PC demand.

- HBM-blended DRAM, used in AI accelerators, sustains even stronger pricing momentum.

- NAND Flash prices remain elevated at ~33–38% QoQ, reflecting supply optimisation for enterprise SSDs.

What this implies

Price increases are occurring even where market fundamentals would normally suggest moderation.

TrendForce notes that while notebook and consumer electronics demand remains constrained, suppliers are actively limiting shipments to these channels. Capacity is instead funnelled toward customers able to commit to large, long-term, high-margin contracts — primarily hyperscalers and AI infrastructure operators.

To make this divergence explicit, the chart below compares projected 1Q26 contract price increases by segment, using only TrendForce-reported values.

{

"data": [

{

"x": ["Server DRAM", "Conventional DRAM", "Client SSD"],

"y": [60, 57.5, 40],

"type": "bar",

"text": [

"AI servers and CSP capacity pre-booking",

"Shipment controls despite weak PC demand",

"NAND output redirected to enterprise SSDs"

],

"hovertemplate": "%{x}<br>%{y}% QoQ increase<br>%{text}<extra></extra>"

}

],

"layout": {

"title": {

"text": "Projected 1Q26 Memory Contract Price Increases by Segment (TrendForce)"

},

"yaxis": {

"title": "Quarter-on-Quarter Price Increase (%)",

"rangemode": "tozero"

}

}

}

Methodology note: Conventional DRAM uses the midpoint of the reported 55–60% range. No extrapolation beyond published data has been performed.

Conclusion: the consumer memory market is no longer optimised for stability or affordability. It is increasingly treated as residual output of an industry tuned for AI workloads.

What consumers will actually experience

The exit of Crucial has immediate, practical consequences:

- fewer affordable memory options

- higher baseline prices for upgrades

- reduced competitive pressure in the mid-range

According to Tom’s Hardware, NAND production costs have risen sharply, pushing SSD and RAM prices upward across consumer segments.

Source: Tom’s Hardware, RAM and SSD prices will continue to rise https://www.tomshardware.com/pc-components/ram/dont-wait-if-youre-planning-to-upgrade-your-ram-or-ssd-kingston-rep-warns-says-prices-will-continue-to-go-up-nand-costs-up-246-percent

This disproportionately affects:

- students

- freelancers

- small studios

- mainstream laptop buyers

Revenue follows AI

Micron’s decision reflects where revenue growth is now concentrated.

Based on earnings calls and Reuters financial analysis, data centre and AI-related memory now account for a rapidly growing share of revenue, while consumer segments stagnate.

Micron revenue focus: consumer vs data centre (qualitative shift)

{

"data": [

{

"type": "bar",

"name": "Consumer Memory",

"x": ["Past (Pre-AI boom)", "Current"],

"y": [1, 0.5]

},

{

"type": "bar",

"name": "Data Centre & AI",

"x": ["Past (Pre-AI boom)", "Current"],

"y": [0.6, 1.2]

}

],

"layout": {

"title": {

"text": "Relative Revenue Emphasis Shift (Illustrative, Source-Based)"

},

"yaxis": {

"title": "Relative Revenue Weight (Indexed)"

},

"barmode": "group"

}

}

Important clarification: this chart is illustrative, reflecting directional emphasis described in earnings calls rather than exact revenue percentages.

Counterargument: what if AI demand slows?

A common counterargument is that AI infrastructure demand may normalise, freeing capacity back to consumer markets.

However, this assumes manufacturers are willing to retool advanced process nodes for lower-margin consumer products — an assumption not supported by current capital allocation trends. Once fabs, contracts, and roadmaps are optimised for hyperscale customers, reversion is economically unattractive.

The hidden risk of over-concentration

The semiconductor industry is historically cyclical.

By concentrating production and investment almost entirely on AI and enterprise demand:

- flexibility decreases

- exposure to demand normalisation increases

- consumer trust erodes

Crucial’s exit is therefore not merely a cost decision, but a strategic bet on the durability of AI-driven demand.

Conclusion: Crucial is a symptom, not the disease

Crucial did not disappear because it failed. It disappeared because it no longer fit an industry optimised for AI margins.

For consumers, this likely means:

- higher prices

- fewer choices

- longer upgrade cycles

The memory market is being reshaped in real time. The more relevant question may be whether the consumer memory segment will ever again be treated as a first-class priority in a post-AI semiconductor industry.

Sources

- Micron Investor Relations — https://investors.micron.com/

- Reuters, semiconductor and memory market analysis — https://www.reuters.com/

- TrendForce, memory pricing reports — https://www.trendforce.com/

- Tom’s Hardware, component pricing commentary — https://www.tomshardware.com/

If you found this useful, please cite this as:

Rossetti, Simone (Jan 2026). The End of Crucial: How the Memory Industry Is Abandoning the Consumer Market. https://rossettisimone.github.io.

or as a BibTeX entry:

@article{rossetti2026the-end-of-crucial-how-the-memory-industry-is-abandoning-the-consumer-market,

title = {The End of Crucial: How the Memory Industry Is Abandoning the Consumer Market},

author = {Rossetti, Simone},

year = {2026},

month = {Jan},

url = {https://rossettisimone.github.io/blog/2026/the-end-of-crucial/}

}

Enjoy Reading This Article?

Here are some more articles you might like to read next:

Subscribe to be notified of future articles: